Key Takeaways

- Long term loans in Singapore allow borrowers to spread repayments over an extended period, reducing monthly financial strain.

- A loan with long term payment terms is suitable for major expenses such as education, home renovations, or business financing.

- Common types of long term loans include personal loans, debt consolidation loans, education loans, renovation loans, and business loans.

- Banks generally offer lower interest rates but stricter approval criteria, while licensed money lenders tend to provide faster, more flexible options.

- Although longer repayment tenures can lower monthly instalments, they may increase total interest paid, so affordability should be carefully considered.

- Borrow only from licensed lenders and ensure you understand your rights under Singapore’s Moneylenders Act before committing to a loan.

Long term loans are financing options that allow borrowers to spread repayments over an extended period, making monthly instalments more manageable. A loan with long term payment terms is commonly used for big-ticket expenses like higher education, home renovations, medical bills, or business costs.

In Singapore, you can get long term personal loans from both banks and licensed money lenders; however, bear in mind that the terms, approval requirements, and repayment structures can vary significantly. In this guide, we explore safe and regulated borrowing options, helping you understand the various types of long term loans available, how repayment works, the advantages and risks involved, and tips on choosing the right loan for your financial situation.

If you’re comparing borrowing options, our guide on personal loans in Singapore might also be helpful.

What Are Long Term Loans?

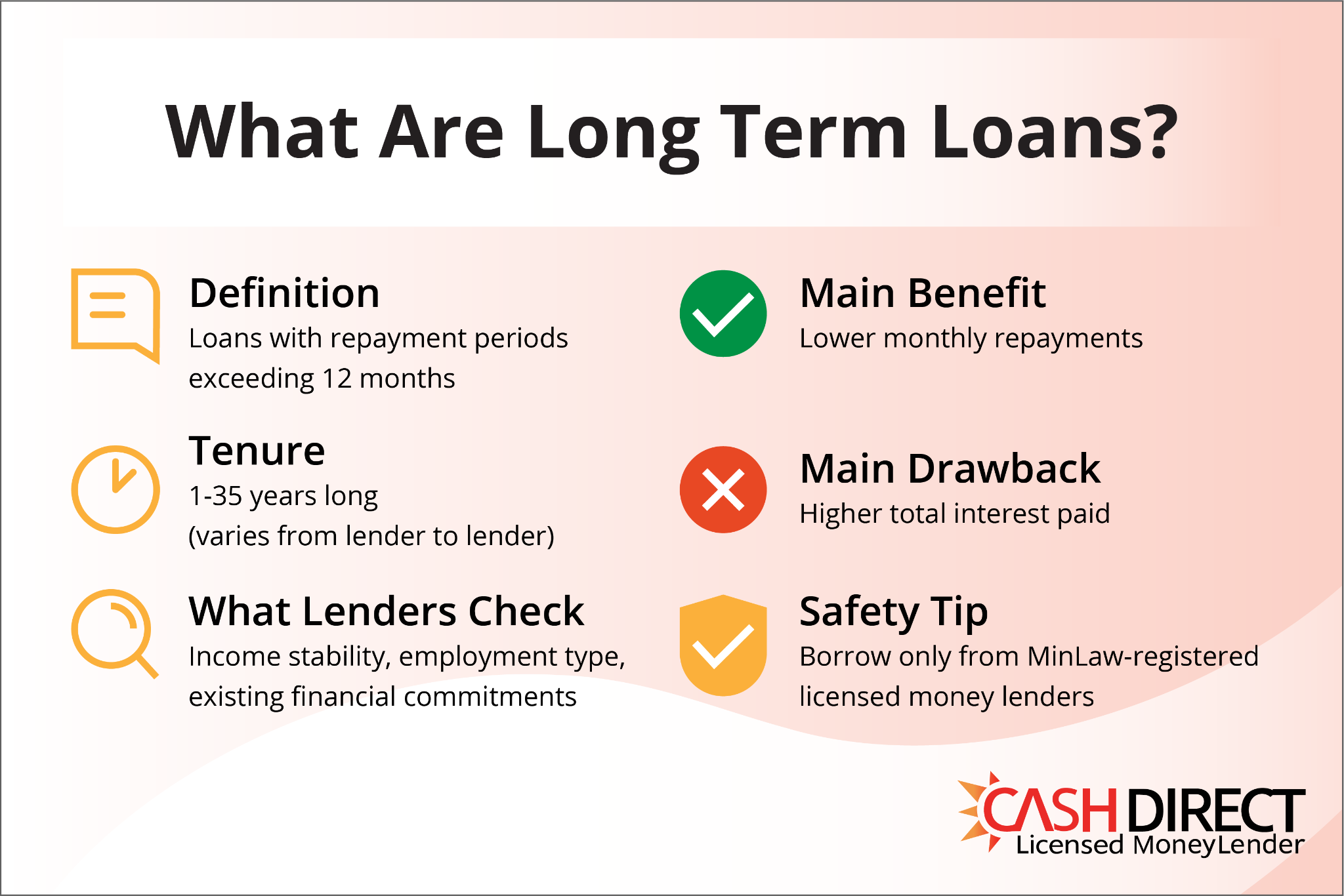

Long term loans are loans with repayment periods that typically exceed 12 months. Depending on the lender and type of loan,, repayment tenures can range from one year to as long as 35 years.

By spreading repayments over a longer period, long term loans help lower monthly instalment amounts, making them easier on the wallet for borrowers. However, keep in mind that a loan with long term payment arrangement usually incurs higher total interest than a loan with a shorter repayment period.

When evaluating long term loan applications, lenders consider factors such as income stability, employment type, and existing financial commitments. In Singapore, both banks and licensed money lenders are required by law to assess a borrower’s ability to repay before approving any loan.

Always ensure that any loan with long term payment arrangement is taken from a lender listed on MinLaw’s official list of registered money lenders. This helps protect you from illegal lenders and ensures your loan is regulated and legitimate.

Types of Long Term Loans Available in Singapore

There are different types of long term loans designed to suit various financial needs. Selecting the most suitable option depends on your reasonfor borrowing, income level, and repayment capacity.

#1 Long Term Personal Loans

Long term personal loans are designed for general purposes and typically offer flexible repayment tenures, usually up to seven years. Repaid through fixed monthly instalments, these loans with long term payment arrangements make budgeting easier and suit both salaried and self-employed individuals. The interest rates for such long term personal loans vary by lender and borrower profile, so comparing current loan interest rates can help you find the most cost-effective option.

Advertised personal loan rates from major banks start from as low as 1.08%-1.8% per annum, with effective interest rates around 2.09%-3.5% per annum once fees and charges are included. On the other hand, licensed lenders cap interest at 4% per month (up to 48% per annum) and usually offer shorter tenures of up to 1 year (some lenders may offer tenures of up to 2 years on a case-by-case basis). While this makes the total cost of borrowing higher than a bank loan, licensed lenders provide faster access to funds and flexible options for borrowers who may not meet a bank’s stringent eligibility criteria.

#2 Debt Consolidation Loans

Debt consolidation loans allow borrowers to merge multiple unsecured debts into a single loan with one monthly instalment, greatly simplifying repayment and reducing the risk of missed payments. Using a loan with long term payment terms can improve monthly cash flow, especially if you already struggle with managing several high-interest debts.

However, debt consolidation works best when paired with disciplined financial habits to avoid taking on new debts. You can learn more about your options in our debt consolidation loan guide or explore practical strategies for managing debts.

In Singapore, the two main legal ways to consolidate debts into a single monthly repayment are a bank-offered Debt Consolidation Plan (DCP) and a debt consolidation loan from a licensed money lender. A bank DCP, regulated by the Monetary Authority of Singapore, typically offers nominal interest rates from 3.48% per annum (EIR from 6.33% p.a.) and longer repayment tenures of up to 10 years, which can make monthly repayments more manageable and cost-effective overall. That said, not everyone can meet the criteria to qualify for one.

In contrast, a licensed money lender debt consolidation loan, regulated by the MinLaw’s Moneylenders Act, may be easier and faster to qualify for, but with a higher overall cost of borrowing (up to 4% monthly interest and a tenure of 12 months).

#3 Education Loans

Education loans are long term loans designed to fund tuition fees, professional courses, and skills upgrading, often with flexible repayment features such as deferred repayment or a grace period until graduation. By structuring repayments as a loan with long term payment terms, students and families can better manage education-related expenses. Before applying, it’s important to understand when interest starts accruing and how repayments will affect your finances after graduation.

Individuals looking for assistance with school fees in Singapore may consider government-assisted schemes, bank education loans, and education loans from licensed lenders.

Government-assisted schemes like the Tuition Fee Loan (TFL) provided by the Ministry of Education (MOE) generally offer interest rates from around 3.0% per annum and more favourable terms, such as interest-free study periods and much longer tenures of up to 20 years. Education loans from banks typically have slightly higher nominal interest rates starting at 4.38% per annum (additional fees may apply), and shorter tenures of up to 10 years. Both options may require a guarantor, a joint applicant, and/or proof of income, depending on the bank’s specific requirements. Hence, applicants looking for quicker access and fewer eligibility hurdles may find education loans with long term payment terms from licensed money lenders to be a viable option, with interest legally capped at 4% monthly and repayment tenures of up to 1 year, depending on the lender.

#4 Renovation Loans

Transforming your home can be expensive, but renovation loans make it possible for homeowners to bring their dream upgrades to life without paying the full cost upfront. These loans with long term payment terms typically offer repayment tenures of one to five years, spreading the cost over time so monthly finances remain manageable.

While banks in Singapore tend to offer renovation loans with long term payment arrangements with lower nominal interest rates from 4.88% per annum (EIR 5.96% p.a.) and longer tenures of up to five years, they usually require comprehensive documentation and stricter eligibility checks. These loans are strictly only for footing renovation bills — they cannot be used to purchase essentials such as furniture and appliances.

Licensed money lenders, on the other hand, provide renovation loans that are easier to obtain and qualify for. Interest is capped at 4% per month on the outstanding balance, with shorter repayment periods to suit borrowers seeking faster access and more flexible financing options. For the most part, they don’t place any restriction on how the funds are utilised; you are free to use them for buying furniture, fixtures and home appliances.

#5 Business Term Loans

Business term loans are long term loans used to fund business expansion, equipment purchases, working capital, and other operational needs. By extending repayments over a longer period, these loans with long term payment arrangements help businesses maintain stable cash flow and stay financially agile.

Businesses in Singapore can obtain long term loans from banks, government-backed schemes, or licensed money lenders. Bank financing and government-backed schemes, including loans under the Enterprise Financing Scheme (EFS), feature interest rates starting from 7% annually and tenures of up to 5 years. For businesses seeking speedier approval or more straightforward qualification criteria, licensed lenders may be a viable alternative with monthly interest rates at 4-8% and loan tenures of up to 12 months.

How to Choose the Right Loan With Long Term Payment

Choosing the right loan with long term payment terms starts with understanding what you can comfortably repay each month, rather than focusing solely on the loan tenure. Longer repayment periods may reduce your monthly instalments and make them more manageable, but that also means forking out more in interest over the life of the loan.

When comparing loans, consider the interest rates, applicable fees, and total repayment costs across different lenders. It’ll also be prudent to account for your future financial commitments and income stability before committing to long term obligations.

Long Term Loans From Banks vs Licensed Money Lenders

Borrowers looking for long term loans should note that banks are the only institutions that offer true long term loans, typically with repayment tenures extending up to several years or even decades if you’re talking about home loans. Here’s a quick side-by-side comparison to help you understand how bank loans differ from licensed money lender loans:

| Feature | Banks | Licensed Money Lenders |

|---|---|---|

| Loan Tenure | Over 1 year | Typically up to 12 months |

| Interest Rates | Generally lower | Higher, but legally capped |

| Approval Speed | Slower, may take days or weeks | Faster, often within a day |

| Eligibility Criteria | Stricter requirements | More flexible criteria |

| Accessibility | Best for borrowers with strong credit | Suitable for a wider range of borrowers, incl. those with bad credit history |

Before committing, borrowers should carefully compare their options to find the best fit for their needs. For a detailed comparison, refer to our guide on the differences between bank and LML loans.

Risks and Considerations of Long Term Personal Loans

Loans with long term payment terms carry certain risks. Extended repayment periods typically lead to higher total interest, and committing to repayments over many years can create financial pressure if your income changes unexpectedly.

Borrowers should also take the time to scrutinise loan terms carefully, including early-repayment penalties and hidden fees. Borrowing responsibly and working only with licensed lenders are key to avoiding unnecessary stress and long-term financial difficulties.

What Are the Licensed Money Lender Laws That Protect Borrowers?

The Moneylenders Act regulates licensed lenders in Singapore, setting limits on interest rates and fees while requiring transparent loan agreements. Interest is capped at 4% per month on the outstanding balance, regardless of income level, and late interest (if applicable) is also capped at 4% monthly. Fees are regulated as well—any applicable administrative fees cannot exceed 10% of the principal loan amount, and the total interest and fees charged cannot exceed the loan principal.

Licensed money lenders are required by law to provide clear, transparent loan contracts that fully disclose all terms and charges. They are also prohibited from engaging in harassment, intimidation, or unfair practices. Before taking out any loan, always verify that the lender is licensed and listed on the Registry of Moneylenders. For a detailed breakdown of your rights and borrower protections, refer to our guide on licensed money lender rules.

Making the Right Choice for Long Term Loans

Loans with long term payment terms can be a practical financial solution when used responsibly. By understanding the different types of long term loans available, borrowers can select options that align with their financial goals and cash flow needs.

Always assess what you can comfortably afford, compare lenders carefully, and borrow only from licensed institutions. When structured thoughtfully, a loan with long term payment terms can ease financial pressure while helping you meet important life or business needs.

If you’re ready to take the next step, you can apply now, read real customer reviews to learn more about how Cash Direct supports responsible borrowing, or contact us for personalised advice and guidance.

Frequently Asked Questions About Long Term Personal Loans

Can foreigners apply for long term loans in Singapore?

Yes, foreigners can apply for long term loans in Singapore, but eligibility requirements are usually stricter than for Singaporeans or Permanent Residents. Loan amounts may also be limited based on your income, employment type, and the lender’s policies.

Does repaying on time improve my chances of securing a long term loan?

Absolutely. Making consistent, timely repayments not only keeps your loan in good standing but also helps build a positive credit history, which can make it easier to secure future long term personal loans or other types of credit at better rates.

What documents are required when applying for licensed money lender loans?

Most lenders require valid identification (NRIC or work pass), proof of income (salary slips, bank statements, or CPF contribution records), and employment details. Some lenders may also request proof of residence or additional supporting documents, depending on the loan type.

Is early repayment of my licensed money lender loan allowed?

Yes! Unlike banks, licensed money lenders do not charge penalties for early repayment, so you can settle your loan in full at any time without extra costs.