Key Takeaways

- Borrowing limits are regulated, not arbitrary. The amount you can legally borrow from a licensed money lender in Singapore depends on your income, residency status, and government regulations—not the lender’s discretion.

- Income plays a major role in loan eligibility. Higher-income borrowers may qualify for larger loan amounts (up to a multiple of their monthly income), while lower-income individuals are subject to stricter caps for protection.

- Licensed money lenders are safe and regulated. Working with a legal money lender ensures you are protected by Singapore’s laws, including caps on interest rates and fees under the moneylending licensing framework.

- Interest rates and fees are controlled. The licensed money lender’s interest rate is capped (typically at 4% per month), and charges like late fees and admin fees are regulated to prevent excessively high or unreasonable costs.

- Approval depends on more than just income. Factors such as existing debts, repayment ability, and credit behaviour all influence how much you can borrow—even if you meet the basic income and age criteria.

If you’re wondering “How much can I borrow from a money lender?”, the short answer is that most borrowers in Singapore can access a loan amount based on a multiple of their monthly income—subject to eligibility and regulatory limits. In Singapore’s licensed moneylending environment, borrowing is not arbitrary; it is carefully regulated by the government to ensure fairness and prevent over-indebtedness.

This also means that working with a licensed money lender is far safer than dealing with illegal operators when it comes to getting a money loan in Singapore. Licensed lenders operate under strict rules, giving borrowers peace of mind when applying for a money loan in Singapore.

In this guide, you’ll learn about your unsecured loan limit in Singapore, permitted licensed money lender interest rates, fees, and what affects your eligibility. You’ll also discover practical tips to improve your chances of approval and make informed borrowing decisions. Read on now!

Understanding Borrowing Limits From Licensed Money Lenders

In the context of our guide, borrowing limits refer to the maximum amount a licensed money lender is legally permitted to lend to a borrower. These limits are not set by individual lenders but by Singapore’s regulatory authority for licensed money lenders.

The purpose of these limits is to safeguard borrowers from taking on more debt than they can reasonably manage. As part of this process, every licensed lender must assess key factors, including income stability, existing financial obligations, and overall repayment capacity, before approving any legal money lender loan.

Why does this matter? Well, this structured approach is part of the broader system that governs all aspects of licensed money lenders in Singapore, ensuring transparency and responsible lending practices across the industry.

While individuals with stable income may qualify for higher loan amounts, approval is never automatic or guaranteed at the maximum limit—all licensed money lenders in Singapore must check your borrowing limit against the details in your MLCB Loan Information Report.

This is where licensed money lenders differ significantly from illegal loan sharks—they operate within strict regulatory boundaries and conduct proper checks before approving and disbursing funds.

Borrowing Limits by Income and Residency for Unsecured Loans

Wondering about the exact licensed money lender rules pertaining to the unsecured loan limit in Singapore? Take a quick look here:

| Borrower Type | Income Level | Borrowing Limit | Notes |

|---|---|---|---|

| Singapore Citizens & Permanent Residents | S$20,000 or more annually | Up to 6x monthly income (unsecured loans) | Subject to affordability checks and existing financial obligations |

| Below S$20,000 annually | Up to S$3,000 total outstanding licensed money lender loans | Stricter limits to protect financially vulnerable borrowers | |

| Foreigners | Varies (based on income and work pass) | Varies, generally more conservative than locals (e.g. up to S$500 for those earning less than S$10,000 annually) | Depends on work pass type, employment duration, and monthly income |

It’s important to note that these caps apply only to unsecured loans. Secured or specialised loans may have different structures and limits.

Interest Rates and Fees Explained

One of the most common concerns borrowers have is the interest rates charged by licensed money lenders. In Singapore, these rates are strictly regulated and capped at 4% per month (for all loans, excluding business loans), helping prevent excessive borrowing costs.

That’s not all. Interest is calculated on a reducing balance basis, meaning it applies only to the outstanding principal. This ensures borrowers are not paying interest on amounts already repaid, adding transparency and fairness to the entire Singapore money loan process!

Beyond interest rates, there are also standard fees to consider, such as administrative charges (up to 10% of principal) and late payment fees (capped at S$60 per month). These are also strictly regulated to ensure they remain reasonable and do not place undue financial strain on borrowers.

Other things to note

While licensed money lenders generally charge higher interest rates than banks, they are more accessible—especially for those with lower credit scores or urgent cash needs.

Banks, on the other hand, offer lower rates but have stricter requirements and longer processing times. Simply put, not everyone can qualify for a standard bank loan!

Understanding how these rates and fees work can help you better compare options and assess overall affordability.

3 Reasons to Consider Borrowing From Licensed Money Lenders in Singapore

Borrowing from a licensed money lender in Singapore can be a practical solution in several situations.

- #1 More accessible approval criteria: Even if you have a less-than-ideal credit profile, licensed lenders assess more than just your credit score, making them accessible to a wider group of borrowers.

- #2 Fast approval process: If you need funds urgently, approvals can be quick—sometimes within minutes—making them suitable for time-sensitive financial needs.

- #3 Regulated and protected borrowing: All licensed lenders operate under Singapore’s legal framework and must comply with rules set by the relevant authorities overseeing the money lending licensing system, ensuring utmost transparency and borrower protection.

What Are the Factors That Affect Your Loan Borrowing Limits?

Even if you meet the general criteria, the personal loan amount you’re approved for can still vary. Lenders take several factors into account before finalising their decision.

Your income level and its consistency play a major role, as stable earnings signal a greater ability to keep up with repayments. At the same time, any existing debts or outstanding loans are carefully reviewed to ensure you’re not taking on more than you can realistically handle. This is why licensed money lenders never ever promise prospective borrowers the maximum loan amount when giving in-principle approval for their Singapore money loans!

Credit behaviour also carries weight—not just your credit score, but how reliably you’ve managed past financial commitments. On top of that, lenders consider your monthly repayment capacity to make sure the loan remains well within your budget.

The purpose of the loan can also influence the outcome, as different uses may carry different levels of risk. This becomes especially relevant if you’re already juggling more than one financial commitment, since taking on multiple loans can affect both your eligibility and the amount you’re ultimately approved for.

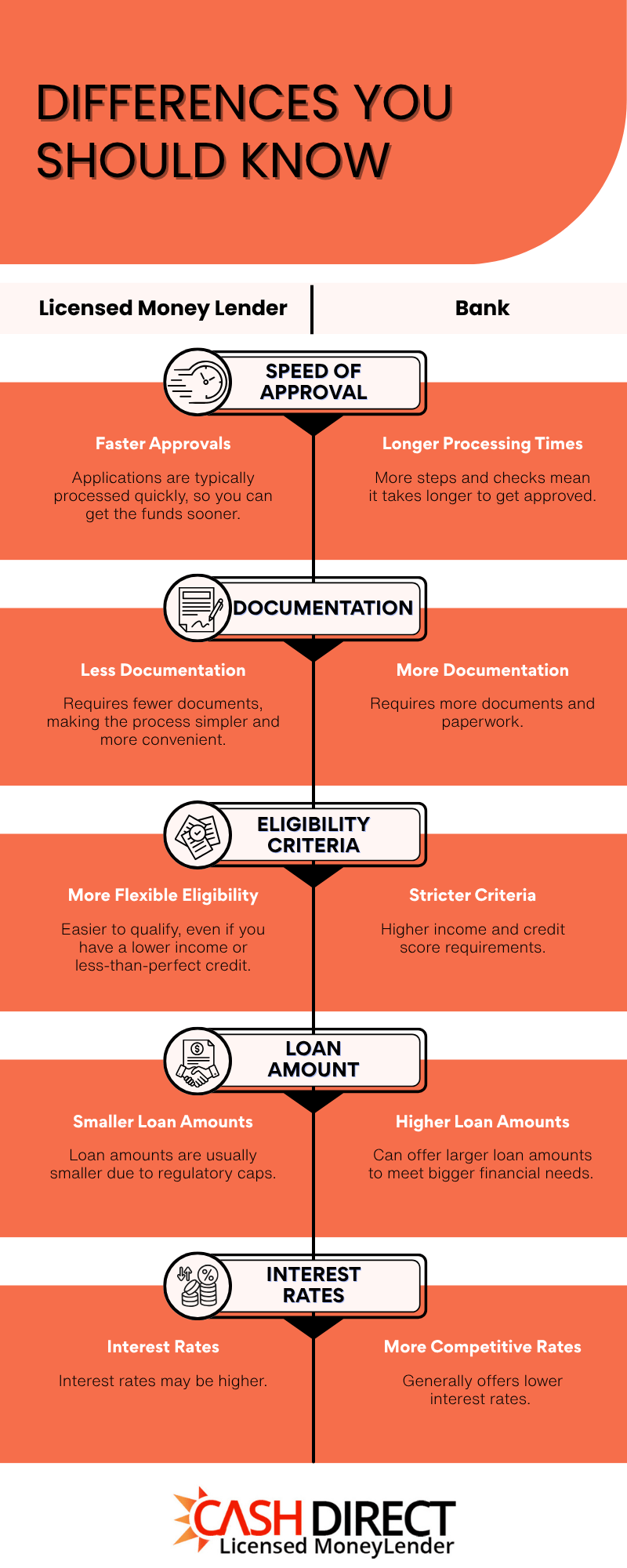

Licensed Money Lenders vs Banks

For borrowers who need funds urgently or may not meet a bank’s requirements, a licensed money lender can be a practical solution. Conversely, if you qualify and are planning for larger financial commitments, banks may offer more cost-effective options in the long run.

Understanding these differences in detail can help you make a more informed borrowing decision, especially when weighing factors like speed, cost, and eligibility.

3 Tips to Improve Your Loan Approval Chances

- Prepare your documents in advance (e.g. income statements and identification) to speed up the process and show reliability.

- Apply only for what you can realistically afford and be honest about your financial situation.

- Avoid submitting multiple loan applications at the same time, as it may hurt your creditworthiness.

Conclusion

Understanding how much you can borrow from a money lender depends largely on your income, residency status, and Singapore’s regulatory framework. With clearly defined borrowing limits and capped interest rates, licensed money lenders operate under strict guidelines designed to keep loans fair, transparent, and manageable for borrowers.

Is a licensed money lender safe to get a loan from? Yes, choosing a licensed money lender is a safe, regulated option, as long as you pick the right lender, borrow responsibly and stay within your financial means. For those who require quick access to funds, established lenders such as Cash Direct—conveniently located just a short walk from Jurong East MRT station—offer a straightforward online loan application process, making it easier to secure financing when it’s needed most!

Before applying, borrowers are encouraged to review past customer testimonials to better understand real experiences and service quality. Those who wish to learn more can contact Cash Direct directly for personalised guidance or explore the available articles and resources to make more informed borrowing decisions.