Key Takeaways

- The updated Moneylenders Act was introduced in 2008 to clarify licensing requirements and adopt a more flexible, forward-looking approach to moneylending regulation.

- Only licensed money lenders listed in the Registry of Moneylenders are permitted to offer loans to the public.

- The law caps interest rates, fees, and late charges to prevent excessive debt and unfair lending practices.

- Borrowers are protected against harassment, intimidation, and misleading conduct, all of which are strictly prohibited by law.

- Always verify a lender’s licence before applying, and borrow only what you can comfortably repay.

The Moneylenders Act is a key piece of legislation that regulates moneylending in Singapore and protects borrowers from unfair practices. Originally enacted in 1959 and strengthened through major reforms in 2008, the Act sets out clear rules to protect borrowers’ interests, including who may lend money, how much may be charged, and the rights borrowers have when dealing with a Singapore money lender. For anyone considering a loan, understanding the Moneylenders Act framework in Singapore is essential for borrowing safely and responsibly.

One of the most important reasons this law exists is to ensure borrowers deal only with licensed money lenders, rather than falling victim to illegal or abusive loan providers. Choosing a regulated lender helps safeguard both your finances and personal well-being.

What Is the Moneylenders Act in Singapore?

The Moneylenders Act is the primary law governing moneylending activities in Singapore. Its purpose is to protect borrowers and ensure that licensed lenders operate ethically and transparently. By setting out clear rules on interest rates, fees, and debt collection practices, Singapore’s Moneylenders Act creates a safer borrowing environment.

Who Is Allowed to Lend Money In Singapore?

Not everyone is legally allowed to lend money in Singapore—the Moneylenders Act clearly specifies three main categories of legal lenders:

#1 Licensed Money Lenders

These are private lending businesses authorised by the Registry of Moneylenders, which operates under the Ministry of Law. They must follow strict regulations covering interest rates, fees, loan contracts, and borrower protections.

#2 Exempt Money Lenders

Exempt money lenders are authorised by the Ministry of Law to operate the business of moneylending under limited, special circumstances. These exempt money lenders have been granted an exemption from holding a licence even though they provide loans to borrowers, typically, specific, limited types of loans. Some examples include Linkflow Capital and Ethoz.

#3 Excluded Money Lenders

Some entities lend money but are not considered commercial licensed money lenders under the Moneylenders Act because they are governed by separate laws or legal frameworks. They do not require a lending license from the Ministry of Law. Examples include:

- Banks and financial institutions, regulated by the Monetary Authority of Singapore (MAS)

- Pawnbrokers, regulated under the Pawnbrokers Act

- Credit societies, governed by the Co-operative Societies Act

- Specialised financial companies that lend to businesses, such as Holistic Enterprise

- Employers providing loans to employees as part of employment arrangements

- Private social lending, such as occasional loans between friends and family, provided it is not conducted as a business for profit

Important: Beware of Unlicensed Money Lenders

Any person or business operating outside the aforementioned categories while engaging in moneylending is acting illegally. Borrowing from unlicensed lenders can expose you to a myriad of serious risks, such as exorbitant fees, harassment, and spiralling debt.

Licensing Rules Under the Moneylenders Act

Legitimate Singapore money lenders are required to hold a licence from the Ministry of Law. To qualify for a licence, money lenders must meet several key requirements:

- Minimum Capital: New licensed money lenders must have at least S$100,000 in paid-up capital.

- Knowledge Test: Key personnel, such as managers, must pass a formal written test on the Moneylenders Act and Rules to demonstrate their understanding of legal responsibilities and best practices.

- Background Checks: Directors and shareholders must undergo stringent background checks to confirm good character and the absence of criminal records.

By enforcing strict licensing rules, borrowers are protected from potential abuse and risks associated with borrowing from unregulated sources.

Interest Rates and Fees Allowed by the Moneylenders Act

The Moneylenders Act Singapore imposes stringent limits on what licensed lenders can charge, ensuring borrowers are protected from exorbitant costs and hidden fees.

Maximum Interest Rate

Licensed money lender interest rates —excluding business loans— have a ceiling of 4% per month, calculated on a reducing balance method basis. This means interest is only applied to the outstanding loan amount, not the original principal—unlike a flat-rate loan. Similarly, late interest is capped at 4% per month, but applies only to overdue payments—not the entire loan balance.

Permitted Fees

Beyond interest, licensed lenders can only charge the following fees:

- Administrative Fee: One-time fee of up to 10% of the loan principal, deducted from the principal at the time the loan is granted.

- Late Fee: Capped at S$60 for every month of overdue repayment.

- Legal Costs: Only recoverable if awarded by a court in debt recovery proceedings.

Any other fees—such as membership fees or early repayment charges—are illegal.

Total Charges

All interest and fees combined, including late charges and administrative fees, cannot exceed the original loan amount. For example, if you borrow S$5,000, the lender should not collect more than S$5,000 in total interest and fees, even if you miss repayments for an extended period of time. This rule prevents borrowers from falling into spiralling debt.

Borrower Rights Under the Moneylenders Act

Borrowers are entitled to robust protections under the Moneylenders Act and the Debt Collection Act:

Advertising Rules

To protect borrowers from misleading or aggressive marketing, licensed lenders in Singapore are subject to strict rules on how they can promote their services:

- No Unsolicited Messages: Lenders cannot send loan offers via SMS, WhatsApp, social media, or email. If you receive such a message, treat it as a red flag for unlicensed moneylending.

- No Random Flyers or Cold Calls: Licensed money lenders are not allowed to distribute flyers in mailboxes or make unsolicited phone calls to promote loans.

- Approved Channels Only: Licensed lenders may advertise only through official, approved channels such as their signage at their registered office premises, their official website, or authorised business and consumer directories.

Clear and Transparent Loan Contracts

Licensed money lenders are required to provide a Note of Contract that outlines all terms, interest rates, and fees before any funds change hands. Borrowers must fully understand the agreement before signing on the dotted line, and lenders must not ask borrowers to sign on blank or incomplete documents. The terms must also be explained in a language that the borrower understands. All licensed lenders are obliged to ensure borrowers know what they are in for before they commit to the legally binding loan.

Right to Documentation

Borrowers are entitled to a full record of their repayments. Every payment, whether made in cash or via bank transfer, must be accompanied by a dated and signed receipt. Lenders are also required to provide an itemised statement of account at least twice a year, which reflects completed repayments and outstanding balances. Additionally, borrowers can request an updated statement at any time, giving them full visibility into their loan.

Protection from Harassment and Abusive Collection Practices

While lenders have the legal right to recover debts, they must operate within the boundaries of the law. Harassment from licensed money lenders is strictly prohibited, including repeated calls at odd hours, threats to friends or family members, and posting debt collection notices outside a borrower’s home. Your personal identification documents—NRICs, passports, or ATM cards—must never be retained by lenders, nor can they demand sensitive information such as Singpass login credentials or bank account details.

Legal Recourse

In the event that a licensed money lender violates borrower rights, borrowers are not without options. Complaints against money lenders can be filed with the Registry of Moneylenders for issues like harassment, overcharging, or unfair contract terms. Legal remedies may also be available under the Protection from Harassment Act (POHA) for cases of harassment.

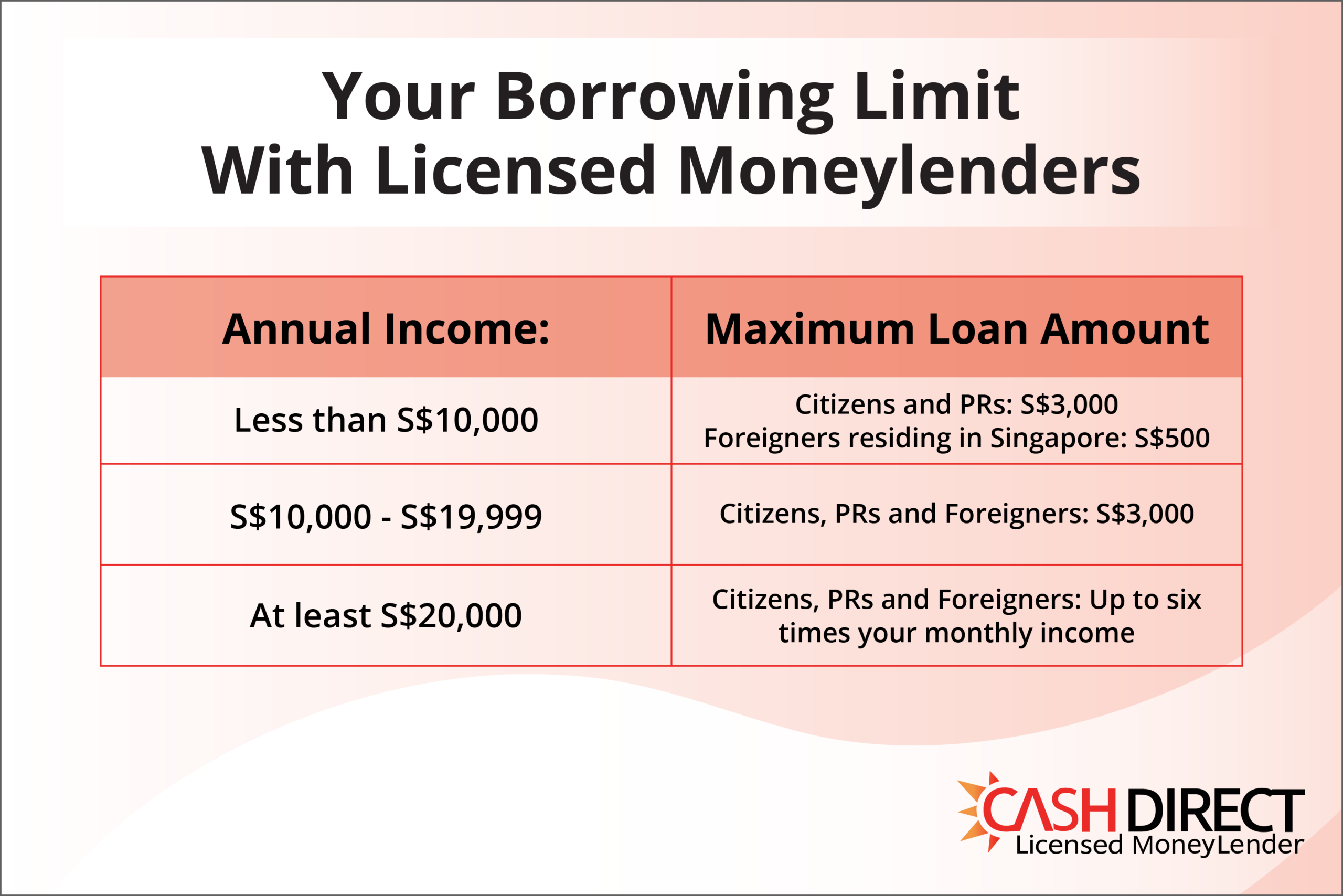

How Much Can I Borrow From a Licensed Money Lender?

How much you can borrow from a licensed money lender depends on your annual income, as outlined below:

How the Moneylenders Act Protects Borrowers in Singapore

The Registry of Moneylenders, maintained by the Ministry of Law, supervises the licensing and regulation of money lenders in Singapore. Beyond licensing, it monitors compliance with the Moneylenders Act and has the power to suspend or revoke licences if a lender breaches any rules. To strengthen regulatory control, the Registry has temporarily suspended the issuance of new licences in recent years.

For borrowers, verifying a lender’s licence before committing to any loan is of utmost importance.

How to Check If a Money Lender Is Licensed in Singapore

The safest way to verify a lender’s legitimacy is to consult the list of registered lenders in Singapore on the Registry of Moneylenders. Make sure the lender’s name, business address, licence number, and contact details match exactly with the Registry listing. To be doubly sure, visit the lender’s registered office and do a check in person!

Be cautious of lenders who:

- Send unsolicited messages or loan offers via WhatsApp or SMS

- Request upfront fees before approving a loan

- Refuse to provide a written loan agreement

Spending a few minutes checking the Registry can protect you from the grave dangers posed by illegal lenders or scammers.

Applying for a Loan From a Licensed Singapore Money Lender

When applying for a loan, you’ll typically need to provide your identification documents, proof of income, and proof of residence. Approval depends on your income and repayment ability.

Before borrowing, always ask yourself: “Can I comfortably manage this loan without overstretching my finances?” Responsible borrowing means only taking what you can afford and fully understanding the loan terms and obligations.

To stay safe, apply through a legal Singapore money lender like Cash Direct, which operates fully within the law and complies with all regulatory requirements in Singapore.

Conclusion

The Moneylenders Act in Singapore provides comprehensive protection for borrowers by regulating interest rates, enforcing licensing rules, and safeguarding your rights. Knowing your rights and understanding the rules can empower you to borrow responsibly and with confidence. Always borrow within your means and choose a licensed money lender you can trust. When you’re ready, reach out to Cash Direct to discuss your options with our friendly loan consultant or start your application online—it only takes a few minutes to kickstart the process.